Buying a home is one of the largest financial decisions you’ll ever make. Discover five practical strategies that can help you make smarter decisions, avoid common pitfalls, and navigate the home-buying process with confidence.

Continue reading

Buying a home is one of the largest financial decisions you’ll ever make. Discover five practical strategies that can help you make smarter decisions, avoid common pitfalls, and navigate the home-buying process with confidence.

Continue reading

Every so often, the calendar gives us a little extra magic—and May 2026 delivers exactly that.

This month brings a rare double feature in the night sky:

Two full moons. One month. And a subtle reminder that timing—whether in nature or real estate—can change everything.

🌸 The Flower Moon: Spring at Its Peak

The Flower Moon marks the moment when spring is fully in bloom. Named for the explosion of wildflowers across North America, it’s long been associated with growth, renewal, and momentum.

Sound familiar?

In the Peninsula housing market, this is often when we see:

🔵 The Blue Moon: A Rare Second Chance

Then comes the encore.

A Blue Moon—defined as the second full moon in a calendar month—lands on May 31st. It’s where the phrase “once in a blue moon” comes from… something a little unexpected, a little rare.

And in real estate terms, it mirrors something we see all the time:

A Local Perspective

Here on the Mid-Peninsula, these moons won’t just be symbolic—they’ll be visible reminders.

Catch them rising over the Bay, glowing just above the hills of Belmont and San Carlos, and you’ll see something we’re always talking about with our clients:

The right moment isn’t always the first moment. But when it arrives—you’ll know.

Final Thoughts

Two full moons in one month are rare. So are perfectly timed opportunities.

Whether you’re watching the skies… or watching the market…

May is a month to pay attention. If you’ve been thinking about making a move, we’re always here to help you recognize when your “blue moon” moment shows up.

Helping you make good decisions—when it matters most.

Drew and Christine Morgan are experienced REALTORS and NOTARY PUBLIC located in Belmont, CA, where they own and operate MORGANHOMES, Inc. They have assisted buyers and sellers in their community for over 30 years. Drew and Christine have received the coveted Diamond award, ranking among the top 50 agents nationwide and the top 3 in Northern California by RE/MAX. To contact them, please call (650) 508.1441 or emailinfo@morganhomes.com

For all you need to know about Belmont, subscribe to this blog right here. You can also follow us on Facebook and on X.

This article provides educational information and is intended for informational purposes only. It should not be considered real estate, tax, insurance, or legal advice; it cannot replace advice tailored to your situation. It’s always best to seek guidance from a professional familiar with your scenario.

BROKER | MANAGER | NOTARY

Inherited Home in California under proposition 19? Recently, we were contacted by two families who had inherited their parents’ homes after the passing of the surviving parent. Unfortunately, in both situations, they had not spoken with a real estate professional beforehand, and it appears their attorney may not have been fully up to date on the newer rules.

Both families intended to move into the homes they inherited. However, because certain steps required under California’s Proposition 19 were not completed in time, the properties were reassessed to the current market value for property tax purposes.

As a result, these families—who otherwise would have been able to move into their parents’ homes and retain a much lower tax base—are now facing significantly higher property taxes. In some cases, increases like this can be financially overwhelming, leaving heirs with the difficult choice of either paying the new, higher property tax or selling the property despite wishing to reside in the home.

We felt this was important enough to bring to people’s attention, as these rules can have a major impact on families inheriting property in California. Understanding the requirements ahead of time can help prevent costly surprises and ensure that the available benefits are preserved.

How Proposition 19 Affects Children Inheriting Their Parents’ Property

California’s Proposition 19 significantly changed how property taxes are handled when children inherit real estate from their parents.

For decades under Proposition 58, children could inherit property and keep the parent’s low property tax base—even if the home became a rental or second home. Proposition 19 narrowed those rules considerably.

If a child inherits a parent’s home, the property tax base can only be preserved if three conditions are met:

1. The home must become the child’s primary residence.

The child must move into the property and claim the Homeowners’ Exemption. If the home is kept as a rental, second home, or investment property, it will generally be reassessed to current market value.

2. The tax base transfer now has a limit.

The inherited property can keep the parent’s tax base only up to $1,000,000 above the parent’s assessed value. If the home’s market value exceeds that threshold, the amount above the limit is added to the property’s taxable value.

3. The claim must be filed within one year.

The heir must file the parent-child exclusion claim with the county assessor within one year of the transfer (usually the date of death). If this deadline is missed, the property may be reassessed to the current market value, which can significantly increase the property taxes.

➡︎ This is where many people make costly mistakes. Some heirs never file the claim at all, others miss the one-year deadline, and many confuse it with the two-year window that applies when homeowners transfer their own tax base to a replacement home (see that rule below), under Proposition 19. Understanding the difference is critical to preserving the lower property tax base.

Why This Matters

Many California homeowners purchased their homes decades ago, meaning their taxable value may be far below current market prices. Under Proposition 19, heirs must now decide whether to move into the property, sell it, or accept a potentially large increase in property taxes.

For families planning estates—or for heirs inheriting property—understanding these rules is critical to avoiding unexpected tax consequences.

✓ Carrying Your Property Tax Base to a New Home [Here’s an online calculator]

Another important provision of Proposition 19 allows certain homeowners to transfer their existing property tax base to a new home when they sell their current one.

Homeowners who are 55 or older, severely disabled, or victims of a natural disaster may transfer the taxable value of their current residence to a replacement home anywhere in California. This can significantly reduce property taxes when downsizing or relocating.

To qualify, the replacement home must be purchased or newly constructed within two years of selling the original property.

After purchasing the replacement property, the homeowner should file the Base Year Value Transfer Claim with the county assessor. While the claim can typically be filed up to three years after purchasing the replacement home, filing sooner ensures the tax benefit is applied from the beginning of ownership.

Understanding these timing rules can help homeowners preserve substantial property tax savings when moving to a new home.

Proposition 19 has introduced rules that many families are still learning about—often after the fact. As we’ve seen recently, missing a deadline or not understanding the requirements can lead to property tax increases that could have been avoided with a little planning.

If you or someone in your family may be inheriting a property, or if you are considering selling and transferring your tax base to another home, taking a few minutes to understand the rules ahead of time can make a meaningful difference. If we can ever be a resource to help clarify how these changes may affect you, we are always happy to help.

Other Articles:

About the Authors

Drew and Christine Morgan are the founders of MorganHomes, their independent brokerage based in Belmont. They also maintain a strategic affiliation with RE/MAX GOLD, combining the flexibility of an independent firm with the resources of one of the largest real estate networks.

As longtime Belmont residents and real estate professionals with more than 30 years of experience, they have helped generations of local families buy, sell, and make smart real estate decisions. Drew is also a Notary Public, providing additional convenience and support for clients when it matters most.

Their consistent performance has earned them RE/MAX’s prestigious Diamond Award, placing them among the top agents nationwide and among the top performers in Northern California.

If you have questions about the Belmont market or would like to discuss your situation, you can reach them at (650) 508-1441 or info@morganhomes.com.

For ongoing insights about Belmont real estate, local market trends, and community updates, you can subscribe to this blog or follow MorganHomes on Facebook and X.

Disclaimer

This article is provided for educational and informational purposes only. It is not intended as real estate, legal, tax, or insurance advice. Because every situation is unique, we recommend consulting with a qualified professional, like us, to understand your specific circumstances.

Belmont Housing Market: A Little More Choice — But Still Moving Fast

We’re about two-thirds of the way through the first quarter of 2026, and the early read on the Belmont housing market is coming into focus.

Inventory has opened up modestly. So far this year, 39 homes have come to market, compared with 34 during the same period last year — about a 15% increase. Currently, there are 31 properties in the pipeline, including 19 active listings available to buyers and another 10 “coming soon” homes preparing to enter the market. Eight properties are already pending.

At first glance, the increase in listings appears to be good news for buyers. And to a degree, it is — there are slightly more choices than there were a year ago.

But the market’s pace tells a more important story.

Homes that are going pending are averaging just nine days on the market. That’s a clear signal that new inventory is being absorbed quickly. In fact, the buyers we’ve represented this year have still found themselves in highly competitive situations. On the last two homes we pursued, each drew roughly 15 offers.

That combination — more listings, but very fast absorption — suggests that demand remains strong and pricing pressure is holding firm. If the market were softening, we would expect to see homes sitting on the market longer, more price reductions, and fewer competing offers. So far, none of those conditions are showing up in the data.

It’s still early, and there haven’t been enough closed sales yet to draw firm conclusions about pricing trends for 2026. But the early indicators point to a market that remains still seller-leaning, with motivated buyers acting quickly when well-prepared homes come to market.

The takeaway: Belmont buyers may have a few more options this year — but the window to act is still short, and competition hasn’t gone away.

What this means for you depends on your timing and your strategy.

If you’re thinking about buying or selling in Belmont this year, the early trends suggest preparation and positioning matter more than ever. Sellers need to price and present their homes correctly to capture today’s fast-moving demand, and buyers need a clear plan to compete when the right property appears. If you’d like a quick, no-pressure review of your home’s current value, or a strategy session to understand your options in today’s market, feel free to reach out. We’re always happy to share what we’re seeing locally and help you make informed decisions about your next move.

About the Authors

Drew and Christine Morgan are the founders of MorganHomes, their independent brokerage based in Belmont. They also maintain a strategic affiliation with RE/MAX GOLD, combining the flexibility of an independent firm with the resources of one of the largest real estate networks.

As longtime Belmont residents and real estate professionals with more than 30 years of experience, they have helped generations of local families buy, sell, and make smart real estate decisions. Drew is also a Notary Public, providing additional convenience and support for clients when it matters most.

Their consistent performance has earned them RE/MAX’s prestigious Diamond Award, placing them among the top agents nationwide and among the top performers in Northern California.

If you have questions about the Belmont market or would like to discuss your situation, you can reach them at (650) 508-1441 or info@morganhomes.com.

For ongoing insights about Belmont real estate, local market trends, and community updates, you can subscribe to this blog or follow MorganHomes on Facebook and X.

Disclaimer

This article is provided for educational and informational purposes only. It is not intended as real estate, legal, tax, or insurance advice. Because every situation is unique, we recommend consulting with a qualified professional, like us, to understand your specific circumstances.

MorganHomes

Broker | REALTORS | Notary

DRE#01124318 | 01174047

The truth is, both approaches have their merits…

Continue reading

The election year introduced a temporary pause in the ongoing rebound of home sales and prices.

Continue reading

If you’ve been residing in your Bay Area home for over five years, chances are you’ve already surpassed the $500,000 capital gains abatement threshold.

Continue reading

Given the substantial wealth associated with owning property in the Bay Area, it’s rational for sellers to strive for enhanced investment gains and carefully assess the most opportune moment to sell their residences. However, the challenge lies in the limited data available to assist them in reaching a well-founded decision.

Our objective is to adopt a forward-looking futurist strategy to aid individuals in making well-informed decisions while avoiding any reliance on methods like fortune-telling cards or crystal balls, or theories that stand to benefit us personally.

The stability of our real estate values has been influenced by Sellers’ reduced desire to sell their homes, a direct consequence of rising interest rates. This has maintained a state of relative equilibrium in the market compared to recent times.

However, the situation might shift in 2024. More Sellers have postponed selling their properties this year, hoping for a more favorable market next year. This presents a potential issue.

Historical market downturns, like the one in 2007, have seen buyers holding off on purchases for years. When they eventually rejoin the market, they tend to do so simultaneously due to changing conditions that they have in common, resulting in multiple offers and price escalation—a phenomenon observed in 2012 following a housing hiatus.

Sellers could also face this challenge. Previously, when government bond purchases kept interest rates artificially low, and people refinanced at around 3%, the anticipation was that rates would rise when the bond purchases ceased. As predicted, Sellers have now refrained from refinancing and moving due to the prospect of significantly increased mortgage payments.

Given that interest rates have doubled in the past two years, Sellers lack motivation to upsize their homes, considering their mortgage payments would more than double. Property tax hikes further compound this issue. Many Sellers we’ve communicated with plan to wait until 2024 before acting.

In this scenario, if more homes come onto the market while the buyer pool remains static, it could lead to lower home prices in 2024 due to reduced competition for available homes.

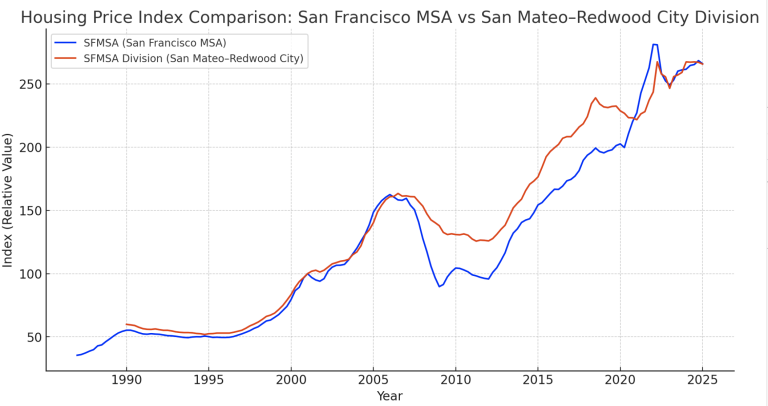

Another challenge in 2024 is the presidential election year, which is historically associated with market pullbacks due to political and economic uncertainties. These uncertainties breed caution and indecision among buyers, particularly from May to November, resulting in further downward pressure on prices.

This graph illustrates the effect the highly contentious election between Hillary Clinton and Donald Trump in 2016 had on home values during those months.

Drawing from historical market trends, we recommend Sellers take proactive measures to address the potential influx of 2023’s home Sellers. Selling before May 2024 becomes crucial for maximizing returns ahead of the election year’s uncertain market conditions.

Drew & Christine Morgan are REALTORS/NOTARY PUBLIC in Belmont, CA with more than 30 years of experience in helping sellers and buyers in their community. As Diamond recipients, Drew and Christine ranked in the top 50 RE/MAX agents nationwide and the top 3 in Northern California. They may be reached at (650) 508.1441 or emailed at info@morganhomes.com.

For all you need to know about Belmont, subscribe to this blog right here. You can also follow us on Facebook and on Twitter.

The information contained in this article is educational and intended for informational purposes only. It does not constitute real estate, tax, insurance or legal advice, nor does it substitute for advice specific to your situation. Always consult an appropriate professional familiar with your scenario.

Drew Morgan, Broker Associate 01124318 | Christine Morgan, Sales Associate—Owners of MorganHomes, Inc. Licensed under RE/MAX Star Properties, 01811140

Contingencies should not be viewed as something you want, they should be regarding as something you need.

Continue reading