Some background

Proposition 13 established initial tax assessments based on property values, which took effect in 1978.

Ad valorem property taxes are currently limited to one percent of a property’s assessed value, plus any voter-approved local taxes such as school or library bonds. Annual increases are limited thereafter to a two percent increase on the property’s compounded value each year.

When a home is sold, the property is reassessed at its current market value. The market value of most properties grows faster than two percent per year, leaving many properties taxed at a value below market price.

How does Proposition 19 change the rules on tax basis portability?

Prop 19 allows a homeowner who is 55 years of age or older, severely disabled or whose home has been substantially damaged by wildfire or natural disaster to transfer the taxable value of their primary residence to: a) a replacement primary residence anywhere in the state, b) regardless of the value of the replacement primary residence (but with adjustments if replacement has a greater value), c) within two years of the sale and d) up to three times (or as often as needed for those whose houses were destroyed by fire).

The prior rule limited this exemption to a one-time transfer within the same county (Prop 60) or between certain counties (Prop 90) and only if the replacement property was of “equal or lesser value.”

When does the tax basis portability portion of Prop 19 take effect?

April 1, 2021

If the replacement property is of equal or lesser value, does the tax basis of the replacement property change?

No. The taxable value of the original property may be transferred and become the taxable value of the new one.

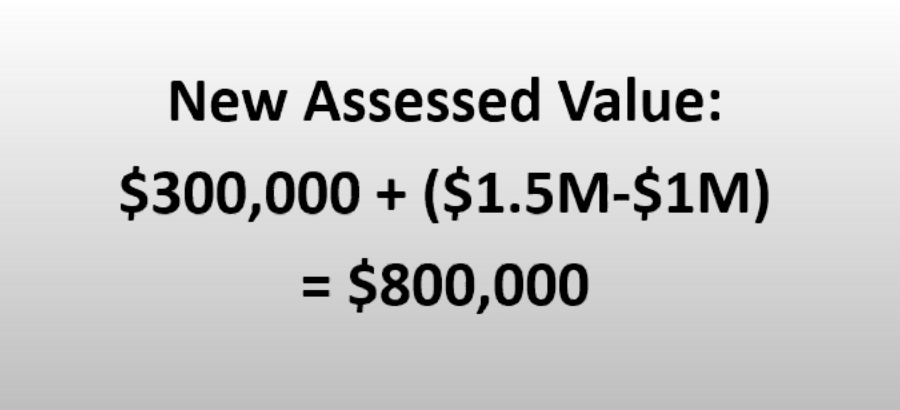

If the replacement property is of greater value, how is the new taxable value calculated?

The new taxable value is calculated by adding the difference between the full cash value of the replacement property and the original property to the original taxable value. For example, if a seller of an original property has a $300,000 taxable value and a full cash value of $1M and then buys a replacement property for $1.5M, the taxable value of the replacement property would be $800,000.

Can a replacement property be purchased before the original primary residence is sold?

Yes. This is how the current rule under Prop 60 works, and Prop 19 uses nearly identical language.

How does Prop 19 affect the rules on intergenerational transfers to children or grandchildren?

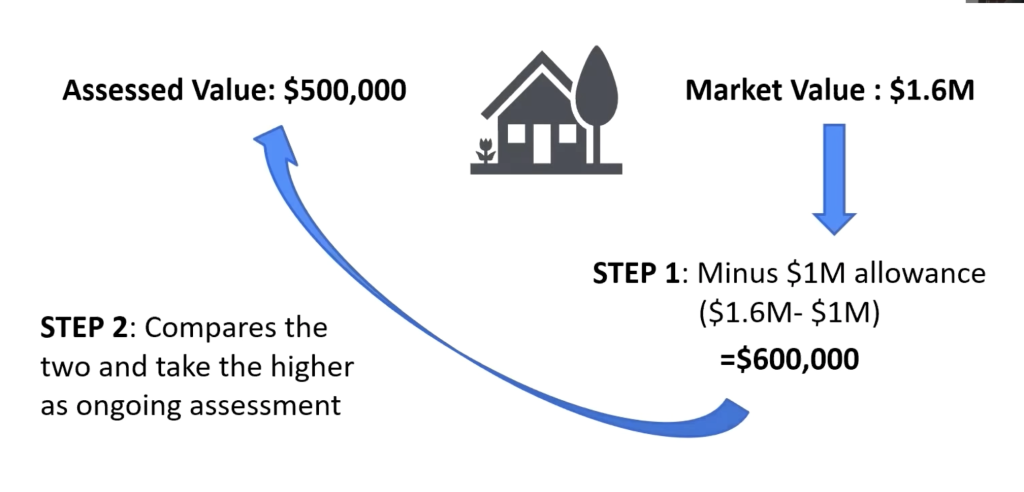

It limits the exemption to those properties where the primary residence continues to be used as a family home by the child or grandchild transferee. If so, the taxable value will remain the same, subject to some upward adjustments if the property value, at the time of transfer, is more than $1M over the original tax basis.

Not a fan of math? Lawyer’s Title now has a handy online calculator to estimate the benefit of carrying your property tax.

If the property is more than $1M over the original tax basis, what is the new taxable basis?

The new taxable basis will be the assessed value of the property at the time of transfer minus $1M.

When do these new rules on intergenerational transfers apply?

February 16, 2021.

Where may a claim to transfer a tax basis be made?

Claims may be made with forms provided by the local county assessor’s office.

What if I don’t yet own a home—how will this help me?

The thinking goes like this. Most people who live in homes they’ve owned for many years could not afford to buy the house where they currently reside, let alone afford the new property taxes.

For example, if one owns a home purchased in 1987 for $150,000, their property tax payment would have started at around $1,875 a year. Thirty years later, assuming the worst-case scenario that the property was reassessed at the maximum 2% each year, their property tax would increase to a minuscule $3,850 per year.

To purchase the same home 30 years later, using the S.F. Metropolitan Statistical Area (MSA) data provided by Case-Shiller, which shows a 1,836% increase in value during that time, our $150,000 house would now cost approximately $2,754,000, with an annual property tax bill of approximately $34,425.00.

It’s rather easy to see why a long-term homeowner would be reticent to make a move.

That could all change.

Homeowners, who previously were likely to stay in place to preserve their low tax base, may now take that base with them, along with their substantial realized equity, to any county in California, opening up a myriad of retirement opportunities that were previously unavailable.

This is where future home buyers could benefit. As more homeowners become aware of the opportunities offered by Prop 19, they can now seek more affordable areas to live. This, of course, could be a boon for new homebuyers, as housing inventory is expected to increase, lessening the frustration of bidding wars and bringing some equilibrium to the market.

If you are a long-term homeowner looking to take advantage of this opportunity, be sure to consult with your tax or legal professional for advice on protecting your options. Additionally, please do not hesitate to contact us if you decide to make a move.

Drew and Christine Morgan are experienced REALTORS and NOTARY PUBLIC located in Belmont, CA, where they own and operate MORGANHOMES, Inc. They have assisted buyers and sellers in their community for over 30 years. Drew and Christine have received the coveted Diamond award, ranking among the top 50 agents nationwide and the top 3 in Northern California by RE/MAX. To contact them, please call (650) 508.1441 or emailinfo@morganhomes.com.

For all you need to know about Belmont, subscribe to this blog right here. You can also follow us on Facebook and on X.

This article provides educational information and is intended for informational purposes only. It should not be considered real estate, tax, insurance, or legal advice; it cannot replace advice tailored to your situation. It’s always best to seek guidance from a professional familiar with your scenario.

BROKER | MANAGER | NOTARY