Ever wondered why you might see a home with sign in the yard and not be able to find it on the internet? Read on. Status symbols and what they really mean.

This can be a bit confusing if you aren’t part of the local multiple listing service so allow me to clarify these terms.

When we list a home for sale is becomes "active" in the MLS system. That’s the first status and it’s referred to as status "1", aptly named. This is when people who have subscribed to automated email alerts generally receive an email announcement that the home has been listed for sale-often times indicated with an [A].

If you see a "Pending Release" or "Pending Sale Release" it typically means an offer was accepted which contains a contingency (usually on the sale of the buyer’s home). This means that the seller has accepted the offer but can release the buyer from the contract if they get another (usually better) offer. This is typically reported as "SALE PENDING RELEASE" or status "2" in the MLS system-also denoted as [PR].

A release clause may be employed in any contract but it’s typically relegated to sales wherein the buyer must sell a home to complete the transaction. Not wanting to be tied up for a protracted period of time, the seller may add a "release clause" to have an option to cancel the contract. Release clauses are typically upon 72 hour notice but they could be whatever the buyer and seller agree upon; and they are typically reserved for when the buyer has a home to sell but again they could be used in any scenario where the buyer and seller agree.

The way a release works is simple. Say you’ve accepted an offer on the home you are selling for $1,000,000, but the buyer must first sell their home to complete the transaction. The seller might agree to your offer but add a release clause stating that upon notification (some point in the escrow period) you have 72 hours to remove the contingency or the seller can then elect to cancel your contract and accept another offer or move a back-up offer into first position-it’s sort of a warning shot across the buyer’s bow if you will. Now let’s say another buyer brings you an offer for $20,000 more after you’re in contract with buyer #1. The first buyer must after written notice either remove their contingency within 72 hours or risk losing the property. So why would a buyer agree to this? Usually because they have no choice. Most sellers insist on this, but secondly the buyer may have sufficient funds in which to close the transaction either in stock or equity but for whatever reason would rather sell their home first. Faced with the 72 release notice, the buyer can then elect to let the home go to another buyer or cash in stocks or their equity and remove the contingency. This way the buyer is not forced into liquidating stocks or paying interest on an equity line of credit until and if necessary.

Status 3 is Pending Sale continue to show. [PS]

This simply means that the seller wants to continue and have their home shown to prospective buyers, and agents. Typically this means there are contingencies in the accepted offer and until they are removed it usually stays in this pending continue to show state. This status is typically reserved during financing and inspection contingencies.

Status 4 is Pending DO NOT SHOW. [PN]

This typically is used when all contingencies have been removed by the buyer but it too can be employed earlier at the seller’s election. This is usually where a property will drop off of the radar by most internet search engines. That’s why you may see a home with a sign in the yard but not be able to find it any longer in the MLS system via the internet.

Status 5 is SOLD and used for when the home has transferred title to the new owners.[S]

Disclaimer: This information is for entertainment purposes only and includes no legal, accounting or real estate advice nor is this response in tended to be specific to your situation-consult a specialist for your specific situation.

Ever wondered why you might see a home with sign in the yard and not be able to find it on the internet? Read on. Status symbols and what they really mean.

This can be a bit confusing if you aren’t part of the local multiple listing service so allow me to clarify these terms.

When we list a home for sale is becomes "active" in the MLS system. That’s the first status and it’s referred to as status "1", aptly named. This is when people who have subscribed to automated email alerts generally receive an email announcement that the home has been listed for sale-often times indicated with an [A].

If you see a "Pending Release" or "Pending Sale Release" it typically means an offer was accepted which contains a contingency (usually on the sale of the buyer’s home). This means that the seller has accepted the offer but can release the buyer from the contract if they get another (usually better) offer. This is typically reported as "SALE PENDING RELEASE" or status "2" in the MLS system-also denoted as [PR].

A release clause may be employed in any contract but it’s typically relegated to sales wherein the buyer must sell a home to complete the transaction. Not wanting to be tied up for a protracted period of time, the seller may add a "release clause" to have an option to cancel the contract. Release clauses are typically upon 72 hour notice but they could be whatever the buyer and seller agree upon; and they are typically reserved for when the buyer has a home to sell but again they could be used in any scenario where the buyer and seller agree.

The way a release works is simple. Say you’ve accepted an offer on the home you are selling for $1,000,000, but the buyer must first sell their home to complete the transaction. The seller might agree to your offer but add a release clause stating that upon notification (some point in the escrow period) you have 72 hours to remove the contingency or the seller can then elect to cancel your contract and accept another offer or move a back-up offer into first position-it’s sort of a warning shot across the buyer’s bow if you will. Now let’s say another buyer brings you an offer for $20,000 more after you’re in contract with buyer #1. The first buyer must after written notice either remove their contingency within 72 hours or risk losing the property. So why would a buyer agree to this? Usually because they have no choice. Most sellers insist on this, but secondly the buyer may have sufficient funds in which to close the transaction either in stock or equity but for whatever reason would rather sell their home first. Faced with the 72 release notice, the buyer can then elect to let the home go to another buyer or cash in stocks or their equity and remove the contingency. This way the buyer is not forced into liquidating stocks or paying interest on an equity line of credit until and if necessary.

Status 3 is Pending Sale continue to show. [PS]

This simply means that the seller wants to continue and have their home shown to prospective buyers, and agents. Typically this means there are contingencies in the accepted offer and until they are removed it usually stays in this pending continue to show state. This status is typically reserved during financing and inspection contingencies.

Status 4 is Pending DO NOT SHOW. [PN]

This typically is used when all contingencies have been removed by the buyer but it too can be employed earlier at the seller’s election. This is usually where a property will drop off of the radar by most internet search engines. That’s why you may see a home with a sign in the yard but not be able to find it any longer in the MLS system via the internet.

Status 5 is SOLD and used for when the home has transferred title to the new owners.[S]

Disclaimer: This information is for entertainment purposes only and includes no legal, accounting or real estate advice nor is this response in tended to be specific to your situation-consult a specialist for your specific situation.

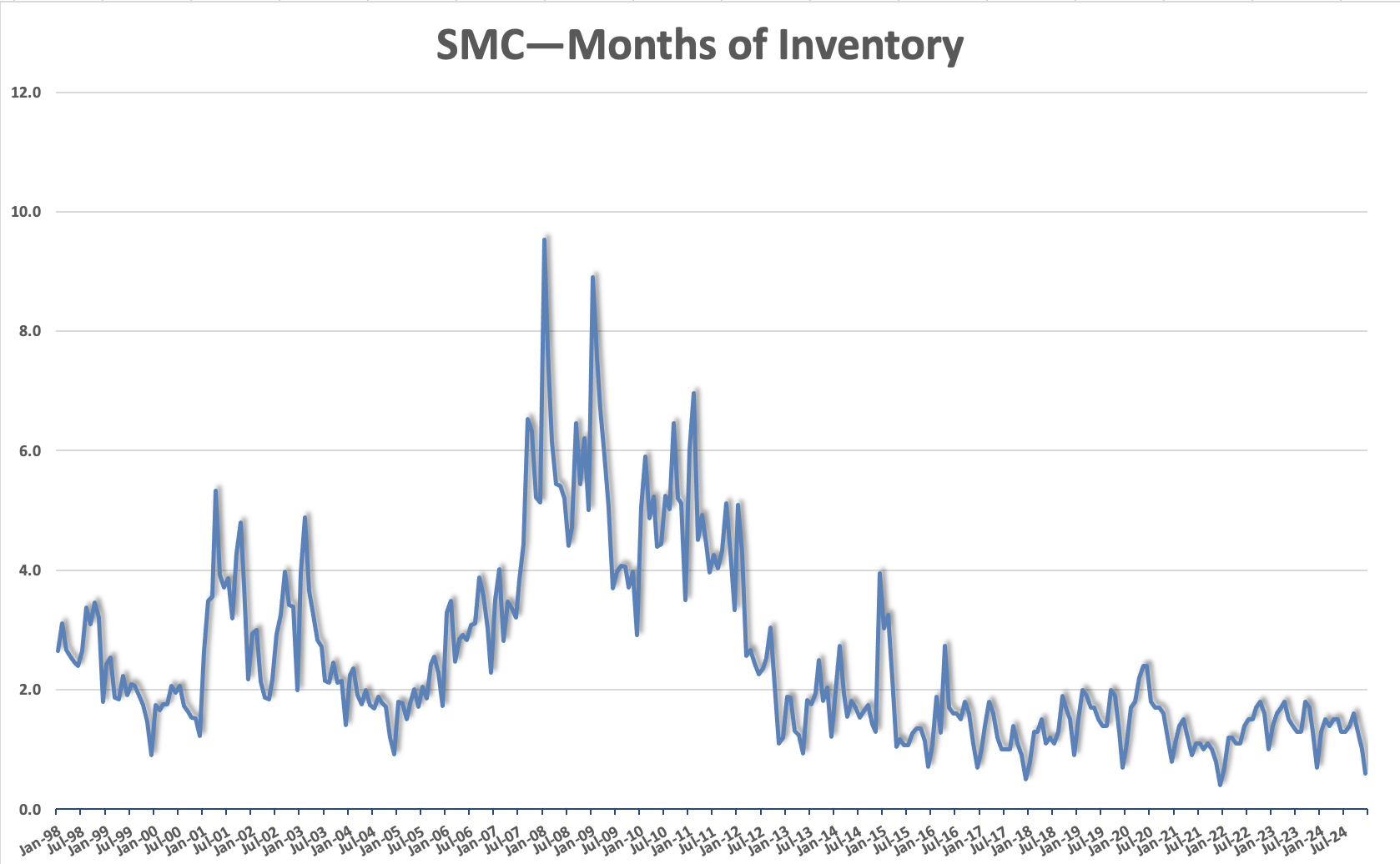

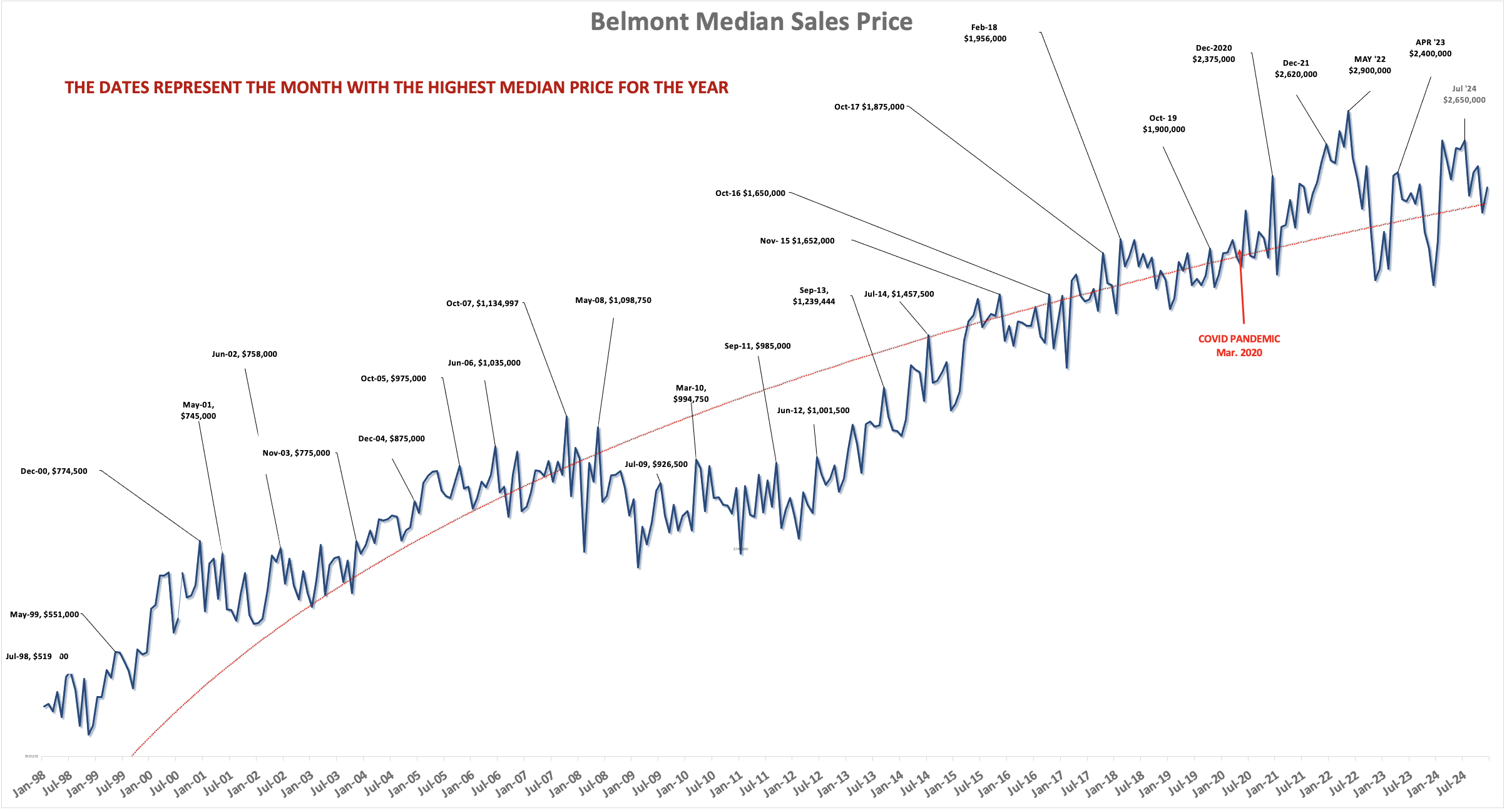

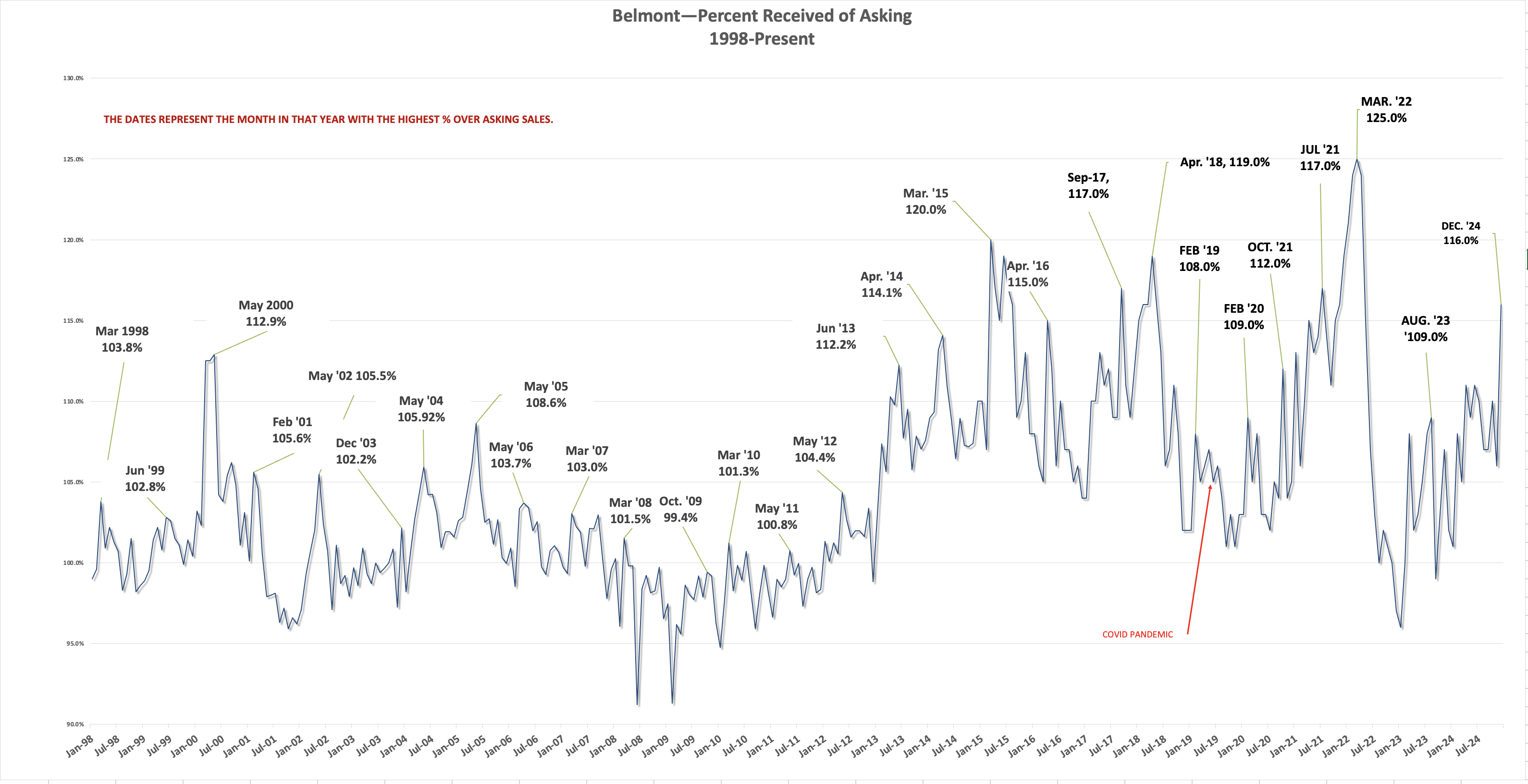

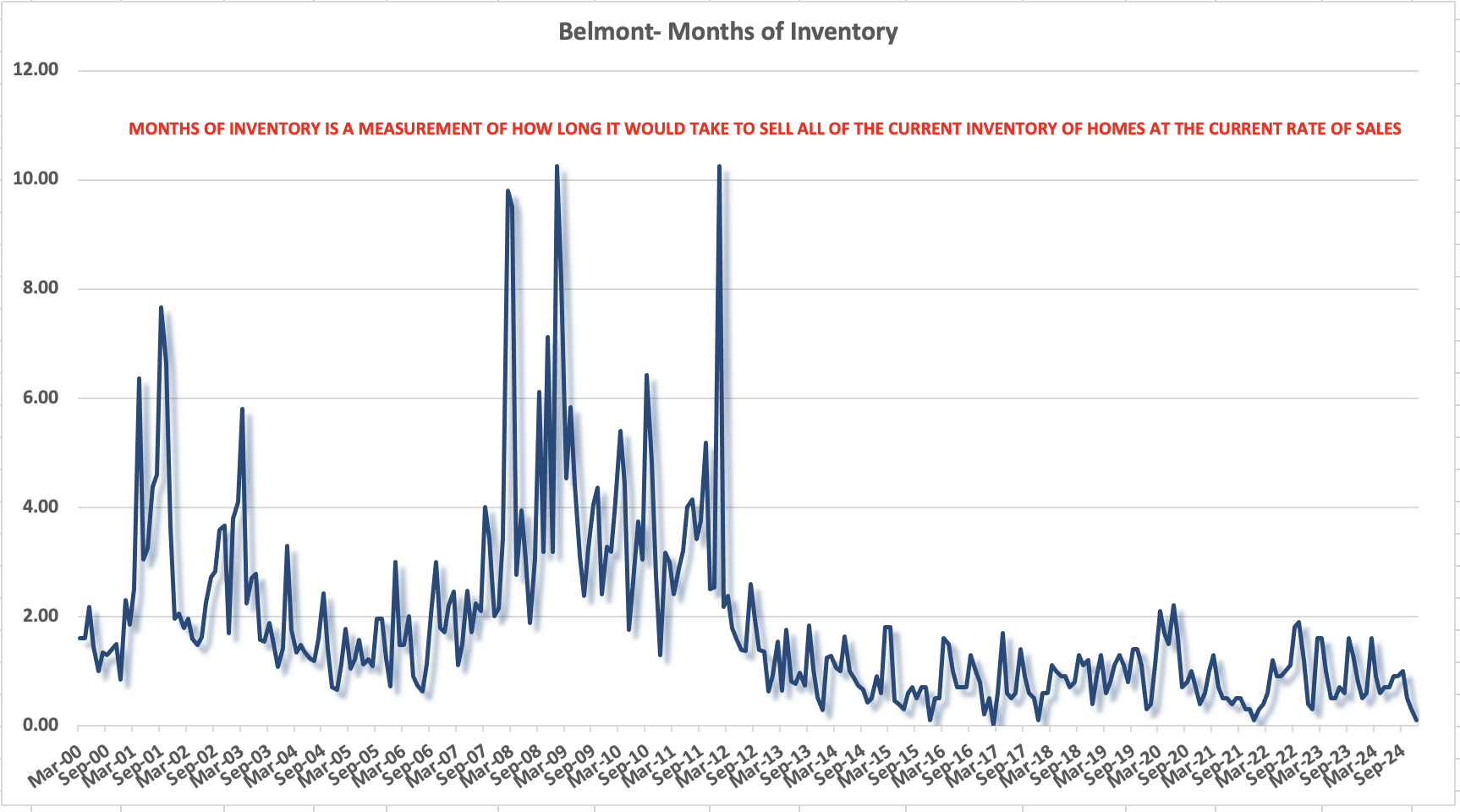

San Mateo County posted a reduction in the median home price to $885,000–a $40,000 (4.3%) decline over $925,000 in 2006.

San Mateo County posted a reduction in the median home price to $885,000–a $40,000 (4.3%) decline over $925,000 in 2006.

The very survival of limited service or virtual Internet brokers relies on two things: The first is they are able to convince everyone that paying a 6% compensation is the only alternative to their "discount" model, and the second is that they must convince their prospects that the minimum service they provide is all that is needed to sell a home; and everything else which a full service agent does is a waste of their time and your money.

The very survival of limited service or virtual Internet brokers relies on two things: The first is they are able to convince everyone that paying a 6% compensation is the only alternative to their "discount" model, and the second is that they must convince their prospects that the minimum service they provide is all that is needed to sell a home; and everything else which a full service agent does is a waste of their time and your money.

{kind=link}