1031 Exchange

Discover The Basics of 1031 Tax Exchanges

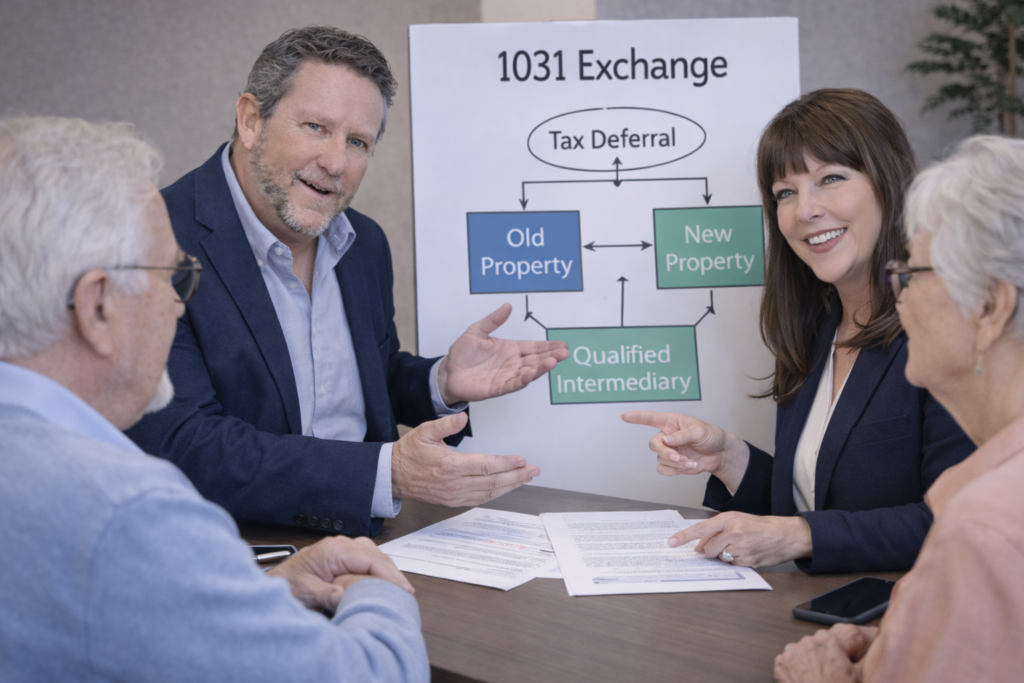

What is a 1031 Tax Exchange?

Things To Know

- An exchange cannot be back dated.

- An exchange cannot be setup after a deal has been closed.

- Any cash withdraw (either in the cash or the form of a note) is called BOOT and will create a taxable event.

- Exchanged properties have a five year holding period before you can take advantage of the home owner’s exemption instead of the normal 2 year holding period

*We are not qualified to give tax or legal advice. You should consult with your attorney and tax specialist before making any decsions regarding a 1031 exchange. If you would like more information on 1031 Exchanges, we would be happy to recommend several 1031 Exchange Companies.

1031 FAQs

In a typical transaction, the property owner is taxed on any gain realized from the sale. However, through a Section 1031 Exchange, the tax on the gain is deferred until some future date. 1031 Exchanges are primarily used for buying and selling investment real estate, but they can also be used for personal property that is used in a business. Some examples of this would include: rental property, office or industrial buildings and vacant land. Just remember that this is tax-deferred, not tax-free.

A 1031 exchange can defer the capital gain taxes that are due on the sale of qualifying properties. By deferring the capital gains, you have more money available to invest in other properties. You can also acquire and dispose of properties to reallocate your investment portfolio without paying tax on any gain.

Both the relinquished property and replacement property must be held for productive use in a trade or business or for investment. Property acquired for immediate resale will not qualify as well as your primary residence.

You have 45 days from the closing of your sale to indentify potential replacement properties. These properties must be identified in writing, signed and delivered to the Qualified Intermediary. There are absolutely no extensions to this deadline so having an agent that can act quickly is of great importance.

From the sale closing date, you have 180 days to close on the purchase of one or more of the identified properties. Again, there are no extensions to this deadline.

The IRS mandates that you use a Qualified Intermediary (QI) to facilitates the tax-deferred exchange. The QI is also sometimes referred to as the Accommodator. The QI is an independant party and can not have any relations to you. The QI holds the sale proceeds until the funds are needed for the replacement property. The main purpose of the QI is to make sure you never have “constructive receipt” of the money. The moment you have “constructive receipt” of the money the exchange is no longer qualified.

You must purchase and take title to replacement propert exactly as you held title to the relinquished property. There are exceptions to this rule however they should be discussed with your CPA and Exchange Company.

The value, equity and debt for the replacement property must be equal to or greater than that of the relinquished property. Also, all of the net proceeds from the sale of the relinquished property must be used to acquire the replacement property.